Yes No

Share to Facebook

Who Pays For the Reduced Value to a Vehicle That Suffers Stigma From An Accident?

Understanding Coverage Applicable to Automobile Accident Damage Requires Careful Review

After providing priority attention to any person injured within an automobile accident, concerns may then turn to the damage to automobiles involved as well as the insurance coverage available to cover the repair costs, the expense of rental vehicle while the repairs are made, or the payout if the automobile is a write-off. Unfortunately, insurance concerns sometimes arise and may become troublesome.

No-Fault Insurance Defined

In Ontario, automobile insurance operates under a no-fault system. Confusingly, no-fault insurance may be misunderstood by some people as meaning that blame or fault is moot in an accident; however, this would be an incorrect understanding whereas the person who is blameworthy for causing an accident is still reviewed and determined. The term no-fault simply means that the determination of who is blameworthy for causing the accident is unnecessary and, generally, irrelevant to the process of making claims for insurance coverage benefits whereas, in nearly all circumstances, where an accident involves an automobile that is registered and insured in Ontario, any claims for damage to the automobile will be claimed against the insurer of the automobile rather than claimed against the blameworthy person.

By making a claim directly to the insurer of an automobile involved in an accident, rather than bringing a legal claim against the person who caused the accident, the intent is that the owner of the automobile will receive the benefits of a more time efficient and cost effective system of insurance. This was well explained by the Court of Appeal in the case of Clarendon National Insurance v. Candow, 2007 ONCA 680 where it was said:

[7] Section 263 of the Insurance Act replaced the tort system that resolved automobile damage claims prior to its enactment. In the new statutory scheme, insureds can no longer sue the tortfeasor driver whose negligence has caused damage to their cars. Rather, their own liability insurer pays for the damage, to the extent that they were not at fault, under the third party liability section of their motor vehicle liability policies. Insureds can recover the at-fault portion of their damage by purchasing collision coverage. Insurers have no right of subrogation for payments to their own insureds, but, on the other hand, do not have to pay the subrogated claims previously brought by other insurers in the tort system. The result is that the statutory regime eliminates the transactions costs that were inherent in the tort system.

As per the Clarendon case, section 263 of the Insurance Act, R.S.O. 1990, c. I.8, disposes of the old tort law system that the owner of an automobile to pursue compensation for damage to an automobile by bringing a tort law claim against the blameworthy person or making a direct claim against the insurer of the automobile and then having the insurer bring a subrogation claim against the blameworthy person. Specifically, section 263 of the Insurance Act states:

263 (1) This section applies if,

(a) an automobile or its contents, or both, suffers damage arising directly or indirectly from the use or operation in Ontario of one or more other automobiles;

(b) the automobile that suffers the damage or in respect of which the contents suffer damage is insured under a contract evidenced by a motor vehicle liability policy issued by an insurer that is licensed to undertake automobile insurance in Ontario or that has filed with the Chief Executive Officer, in the form provided by the Chief Executive Officer, an undertaking to be bound by this section; and

(c) at least one other automobile involved in the accident is insured under a contract evidenced by a motor vehicle liability policy issued by an insurer that is licensed to undertake automobile insurance in Ontario or that has filed with the Chief Executive Officer, in the form provided by the Chief Executive Officer, an undertaking to be bound by this section.

(1.1) This section applies, with necessary modifications, in respect of an automobile the owner, operator or lessee of which is exempt from the requirement to be insured under the Compulsory Automobile Insurance Act, if the organization that is financially responsible for the damages resulting from the accident involving the automobile files with the Chief Executive Officer an undertaking to be bound by this section.

(2) If this section applies, an insured is entitled to recover for the damages to the insured’s automobile and its contents and for loss of use from the insured’s insurer under the coverage described in subsection 239 (1) as though the insured were a third party.

(3) Recovery under subsection (2) shall be based on the degree of fault of the insurer’s insured as determined under the fault determination rules.

(4) An insured may bring an action against the insurer if the insured is not satisfied that the degree of fault established under the fault determination rules accurately reflects the actual degree of fault or the insured is not satisfied with a proposed settlement and the matters in issue shall be determined in accordance with the ordinary rules of law.

(5) If this section applies,

(a) an insured has no right of action against any person involved in the incident other than the insured’s insurer for damages to the insured’s automobile or its contents or for loss of use;

(a.1) an insured has no right of action against a person under an agreement, other than a contract of automobile insurance, in respect of damages to the insured’s automobile or its contents or loss of use, except to the extent that the person is at fault or negligent in respect of those damages or that loss;

(b) an insurer, except as permitted by the regulations, has no right of indemnification from or subrogation against any person for payments made to its insured under this section.

(5.1) Nothing in this Part precludes an insurer, in a contract belonging to a class prescribed by the regulations, from agreeing with an insured that, in the event that a claim is made by the insured under this section, the insurer shall pay only,

(a) an agreed portion of the amount that the insured would otherwise be entitled to recover; or

(b) the amount that the insured would otherwise be entitled to recover, reduced by a sum specified in the agreement.

(5.2) Subsection (5.1) does not apply unless, before the insurer enters into the contract referred to in that subsection, the insurer offers to enter into another contract with the prospective insured that does not contain the agreement referred to in that subsection but is identical to the contract referred to in subsection (5.1) in all other respects except for the amount of the premium.

(5.2.1) In the circumstances prescribed by the regulations, a contract belonging to a class prescribed for the purpose of subsection (5.1) shall provide that, in the event that a claim is made by the insured under this section, the insurer shall pay only the amount that the insured would otherwise be entitled to recover, reduced by a sum specified in the contract.

(5.2.2) Subsection (5.2) does not apply to a contract that contains a provision required by subsection (5.2.1).

(5.3) If a contract contains an agreement referred to in subsection (5.1) or a provision required by subsection (5.2.1), the policy shall have printed or stamped on its face in conspicuous type the words “This policy contains a partial payment of recovery clause for property damage” in English or “La présente police comporte une clause de recouvrement partiel en cas de dommages matériels” in French, as may be appropriate.

(6) This section does not affect an insured’s right to recover in respect of any physical damage coverage in respect of the insured automobile.

(7) This section does not apply to damages to those contents of an automobile that are being carried for reward.

(8) This section does not apply if the damage occurred before the 22nd day of June, 1990.

(9) This section does not apply if both automobiles are owned by the same person.

(10) This section does not apply to damage to an automobile owned by the insured or to its contents if the damage is caused by the insured while driving another automobile.

Fault Determination Rules

As explained above, the term no-fault insurance is often misunderstood as suggesting that blameworthiness for causing an accident is irrelevant and therefore left undetermined; however, such a belief is incorrect. The blameworthiness, or fault for causing an accident, is still determined; however, the determination is irrelevant to where to source certain coverage benefits such as, among other things, loss of income protection when a person is injured in an automobile accident and becomes unable to work and earn. For other coverage concerns, such as coverage for damage to an automobile, where the automobile is insured with collision coverage, among other things, it is still necessary to determine who caused the accident and is therefore the blameworthy person.

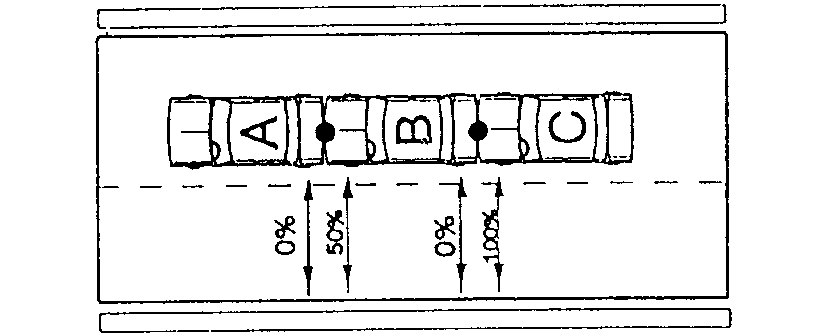

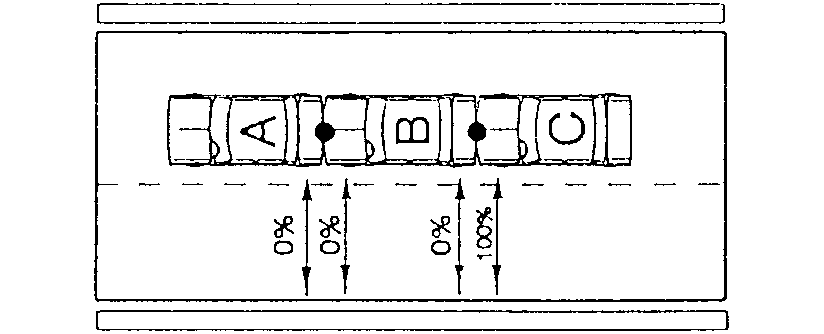

Contrary to urban myth belief, the process of blame or fault determination is completely independent of whether the police lay a charge by issuing a traffic ticket. Instead, the determination of fault is assessed by, in most cases being relatively minor incidents, the insurance adjusters handling review of the insurance aspects of the accident. In almost all circumstances, the determination of fault is a substantially black-and-white issue whether the scenario for the accident is applied to various situations outlined within the Fault Determination Rules, R.R.O. 1990, Reg. 668, as a regulation to the Insurance Act, R.S.O. 1990, c. I.8, both of which are amended regularly. Surprisingly to some, the Fault Determination Rules are primarily pictograms followed with descriptions of a common accident scenario and a prescribed determination of fault based on the pictorialized scenario. As an example, section 9 of the Fault Determination Rules addresses chain reaction rear end accidents involving multiple vehicles:

9. (1) This section applies with respect to an incident involving three or more automobiles that are travelling in the same direction and in the same lane (a “chain reaction”).

(2) The degree of fault for each collision between two automobiles involved in the chain reaction is determined without reference to any related collisions involving either of the automobiles and another automobile.

(3) If all automobiles involved in the incident are in motion and automobile “A” is the leading vehicle, automobile “B” is second and automobile “C” is the third vehicle,

(a) in the collision between automobiles “A” and “B”, the driver of automobile “A” is not at fault and the driver of automobile “B” is 50 per cent at fault for the incident;

(b) in the collision between automobiles “B” and “C”, the driver of automobile “B” is not at fault and the driver of automobile “C” is 100 per cent at fault for the incident.

(4) If only automobile “C” is in motion when the incident occurs,

(a) in the collision between automobiles “A” and “B”, neither driver is at fault for the incident; and

(b) in the collision between automobiles “B” and “C”, the driver of automobile “B” is not at fault and the driver of automobile “C” is 100 per cent at fault for the incident.

As per the example scenario, among others, the Fault Determination Rules statutorily provided for review of the circumstances of an automobile accident and a prescribed assessment of fault. Accordingly, and contrary to perceptions, the determination of fault involves a formal method rather than arbitrariness.

Automobile Insurance, damage coverage sections

Automobile insurance is a uniquely regulated type of insurance whereas, among other things, the coverage is prescribed by law. Simply said another way, the automobile insurance policy and options available are developed by the government; and accordingly, the coverage contract is a standardized document rather than a contract independent worded by different insurers. Of course, it is true that although different insurers are providing the same written contract as automobile insurance policy documents, it is possible that the interpretation and application of the coverage may vary between insurers.

Direct Compensation - Property Damage (DCPD)

As explained above, and with great detail within the Clarendon case, the Direct Compensation Property Damage section of an Ontario Automobile Policy provides coverage that replaces the right to bring a tort law claim against an insured driver who caused the automobile accident resulting in damage to another insured automobile. Whereas section 263 of the Insurance Act contains provisions that bar the right to sue the person who caused an automobile accident, and instead requires that a automobile owner seek compensation from the insurer of the automobile instead, the Direct Compensation Property Damage coverage is, essentially, the substitute for the right to sue.

Uninsured Automobile

When involved in an accident where the driver at fault for the accident was operating an uninsured automobile, a potential coverage gap arises. As above, the Direct Compensation Property Damage coverage is triggered as a replacement to tort rights when an accident is caused by an insured driver; however, if the accident is caused by an uninsured driver, meaning that the vehicle operated by the driver was without insurance per the Ontario Automobile Policy (Owner's Form - OAP 1) or the Ontario Automobile Policy (Driver's Form - OAP 2), then the Direct Compensation Property Damage coverage within the policy of the damaged and insured automobile is untriggered. Accordingly, to fill the gap, and thereby ensure that a responsible automobile owner receives coverage for damage caused by an uninsured automobile, section 5.2.3 of the the Uninsured Automobile section of the Ontario Automobile Policy comes into play. However, and frustratingly victimizing to the owner of the insured automobile, a three hundred ($300.00) dollar deductible applies as well as a twenty-five thousand ($25,000.00) dollar coverage limit. This deductible and limit is often felt as a punishment to the responsible automobile owner who was properly insured yet suffers a damaged automobile at the hands of an uninsured person. While anger is often vented by the responsible automobile owner towards the insurance company, it is actually the government who statutorily imposes this condition. If indeed this circumstance were to happen to you, while you may find that being subjected to a deductible and coverage limit is quite unfair, and reasonably so, any anger and frustration is displaced when directed towards your insurance company as it is the government that must legislate a change.

Collision

As an option coverage, the Loss of Damage Coverage section of the Ontario Automobile Policy (OAP 1) includes Option D for incidents defined as a Collision. As above, where Direct Compensation Property Damage coverage and Uninsured Automobile coverage are protections against accidents caused by the fault of the driver of another automobile, the Collision coverage is what pays for damage occuring as a result of an accident caused by the fault of the driver of the owned automobile (and also applies for a hit-and-run where the other vehicle remains unidentified). Essentially, the Direct Compensation Property Damage coverage and the Uninsured Automobile coverage are protections for accidents caused by someone else and the Collision coverage is protection for accidents caused by you or someone you permitted to drive your automobile. Specifically, a Collision is defined within the policy where it is said:

C. Collision or Upset - we will pay for losses caused when a described automobile is involved in a collision with another object or tips over. Object includes:

• another automobile that is attached to the automobile,

• the surface of the ground, and

• any object in or on the ground.

Interestingly, and humourous to consider, would Collision coverage apply for an insured automobile colliding with a flying aircraft? Whereas the definition of "Object" stated within the Collision definition fails to include an aircraft that is flying over the ground, an interpretation could be that colliding with a flying aircraft is an incident without coverage; however, an alternative interpretation could be that the definition of what type of "Object" is included was just an example shortlist and inexhaustive of all possibilities.

Another point of interest is that the Collision coverage is what will apply when an insured automobile is damaged in a hit-and-run accident where the driver at fault flees and escapes identification. In this situation, an automobile owner incurs any applicable deductible and quite likely feels victimized by an insurance policy that requires a deductible for an accident caused by another, albeit unknown, person.

Avoiding Unnecessary Disputes

When you understand your insurance coverage, and some of the reasons that insurance works the way that insurance works, you may have less of a victimized feeling regarding insurance in general as well as your specific situation. This may help you to rationalize concerns or difficulties and provide some peace within an otherwise frustrating situation.

Actual Cash Value, settlement on loss of automobile

If the damage to an automobile is so substantial as to warrant a write-off settlement rather than a repair, the value of the settlement should be, with two exceptions, the value of the automobile at the time of the loss (minus any applicable deductible). This is known as the "actual cash value". The "actual cash value" is unaffected by the amount still owing on any loans involving the automobile. Additionally, if the vehicle is a write-off, the "actual cash value" applies regardless of the degree of fault assessed for the accident whereas "actual cash value" applies under all three sections applicable to damage arising from an automobile accident, being either the Direct Compensation Property Damage section (see 6.2), the Uninsured Motorist section (see 5.4.4), or the Collision section (see 7.7).

As mentioned, there are two exceptions for when an insurance company may be obligated to pay a sum higher than the "actual cash value" of an automobile. The exceptions are:

- When the insurance policy includes the OPCF#19A endorsement; or

- When the insurance policy includes the OPCF#43 endorsement.

The coverage provided when an Ontario Automobile Policy includes the Ontario Policy Change Form #19A (OPCF#19A) is based on an "agreed value" rather than the "actual cash value" for the settlement of an automobile write-off. Generally, to obtain the OPCF#19A, an insurance company will require an appraisal to confirm that the automobile is worth the amount that the owner is wishing to insure as an "agreed value". If an accident occurs, resulting in the write-off of an automobile insured to an "agreed value" using the OPCF#19A coverage, the difference in value between the "actual cash value" and the "agreed value" is provided by the OPCF#19A coverage.

The coverage provided when an Ontario Automobile Policy includes the Ontario Policy Change Form #43 (OPCF#43 or OPCF#43R for leased vehicles) provides an exception to the usual "actual cash value" that would apply when an automobile is a write-off due to an accident whereas the additional protection waives the depreciation in value that occurs from the time the automobile was purchased (or leased) and the time of the accident. Essentially, the OPCF#43 provides a 'your money back' coverage. The OPCF#43 is usually available for only the first two years from the date of purchase (or lease).

Diminished Valuation, stigma issues

Interestingly, when an automobile is repairable, and the cost of repair is less than the value of the automobile, thus it is financially sensible to repair rather than write-off the automobile, the obligations of an insurer are to make the repairs using like kind and quality parts. Accordingly, where a five year-old automobile is repaired using undamaged parts, whether new or five year-old parts, the five year-old automobile is, or should be, physically, just as good as the automobile was just moments before the accident that caused the damage. Whereas the repaired automobile is, or should be if repaired properly, just as good physically as the automobile was just moments before the accident, it would seem all would be well and satisfactory; however, the market value of vehicle, despite being fully and properly repaired, may be diminished by the stigma of involvement in an automobile accident. Simply said, the selling or trade-in price of two automobiles of the same year, the same make, the same model, and with other attributes such as features and mileage, among other things, also all being the same, may differ if one of the automobiles was involved in an accident whereas an accident experienced automobile is stigmatized despite full and proper repair.

Recently, the question of whether an insurer should be liable for diminitive value loss to an automobile due to the stigma of involvement in an accident was raised within the case of Zheng v. Certas Home and Auto Insurance Co., 2019 ONSC 2753 wherein the statutory coverage prescribed with the Ontario Automobile Policy (OAP #1, Owner's Form) was reviewed and it was stated:

[33] The OAP is not an ordinary contract negotiated between private parties. It is a standard contract imposed by the provincial legislature upon the automobile insurance industry and members of the Ontario public who own motor vehicles. It is not a typical contract of insurance drafted by the insurer. Certas did not select the wording used in the OAP. For that reason, Deputy Judge Da Silva ruled that the principle of contra proferentem should not be applied in interpreting the OAP. Ms. Zheng conceded the correctness of that ruling at the appeal hearing.

[34] The primary rule of construction in interpreting any contract (including an insurance contract) is to give effect to the intention of the parties, as expressed by the words they have used in the contract: Consolidated-Bathurst v. Mutual Boiler, 1979 CanLII 10 (SCC), [1980] 1 SCR 888 at p.899. According to this rule, courts must interpret contract language in the manner that best promotes the shared intent of the parties at the time of entry into the contract.

[35] In the case before me, where the provisions of the insurance contract are mandated by law, a search for the contracting parties’ intention would be a meaningless exercise. Interpretation of the OAP is more akin to statutory interpretation than contract interpretation in so far as it necessitates consideration of legislative intent. The OAP must be construed in a manner consistent with the purposes of the Insurance Act pursuant to which it was enacted. Those purposes include reduction in automobile insurance premiums by eliminating the transaction costs that were inherent in the tort system prior to the introduction of no-fault insurance in Ontario: Clarendon National Insurance, at para.7.

[36] Interpreting the OAP is not, however, a pure exercise in statutory interpretation. Some of the established rules of contract construction still apply, notwithstanding that the OAP is a mandated standard policy. Specifically, there are a number of interpretive principles that courts have developed to address a concern for consumer protection in the insurance industry. In particular, a person who purchases insurance ought to know the scope of the coverage for which they are paying. The Supreme Court of Canada has therefore ruled that words in insurance contracts must be given their plain and ordinary meaning. The OAP must be construed as it would be understood by the average person applying for insurance: Co-operators Life Insurance Co. v. Gibbens, 2009 SCC 59 (CanLII), [2009] 3 SCR 605 at para.21.

[37] As noted above, Deputy Judge Da Silva concluded that Certas exercised its right to repair Ms. Zheng’s vehicle. My task is to determine whether that conclusion reflected an erroneous interpretation of s.6.6 of the OAP, contrary to the applicable rules of construction. This is a question of mixed fact and law.

[38] Questions of mixed fact and law lie along a spectrum. The stringency of the applicable standard of review depends upon where the question falls along that spectrum. As the Supreme Court of Canada stated in Housen, at para.32, “the numerous policy reasons which support a deferential stance to the trial judge's inferences of fact, also, to a certain extent, support showing deference to the trial judge's inferences of mixed fact and law.” However, where a legal principle is not readily extricable from the factual inferences to be drawn, then the matter is subject to the more stringent standard of correctness. “The general rule is that, where the issue on appeal involves the trial judge's interpretation of the evidence as a whole, it should not be overturned absent palpable and overriding error.” Housen, at para.36.

[39] The question for me to determine is not simply whether Deputy Judge Da Silva erred in his assessment of the evidence as a whole when he reached the factual conclusion that Certas had exercised its option to repair Ms. Zheng’s vehicle. That factual issue is intertwined with the legal question of whether Deputy Judge Da Silva applied the proper principles of construction to the OAP. If he erred in his interpretation of the OAP – a statutorily mandated insurance policy -- then he committed an error of law that was inextricably linked to his factual finding. The higher standard of correctness therefore applies to my review of this issue.

[40] For the reasons that follow, I find that the trial judge correctly interpreted the OAP and correctly determined that Certas had exercised its right to repair Ms. Zhen’s vehicle, within the meaning of s.6.6 of the OAP.

[41] Certas concedes that it did not provide Ms. Zheng with written notice of its decision to repair her vehicle. Section 6.6 of the OAP states that the insurer “will let [the insured] know in writing within seven days of receiving notice of the claim” if it chooses to repair, replace or rebuild the automobile rather than pay for the damage.

[42] Ms. Zheng argues that Certas’s failure to provide her with formal written notice of an election is evidence that Certas did not in fact make an election to repair. This argument conflates the issue of whether an election was made with the issue of whether notice was given of that election. The plain meaning of the words in s.6.6 of the OAP make it clear that these are two distinct issues.

[43] Section 6.6 does not stipulate that written notice is a pre-condition to the insurer’s exercise of its right to repair a vehicle. The ordinary meaning of the words in s.6.6 make it clear that the requirement for written notice arises only after an insurer has made an election to repair. In that regard, the wording in s.6.6 of the OAP may usefully be contrasted with the wording of s.1.7.3, which states:

In case of non-payment of premium, we may give you a notice in writing. We must give you ten days notice if we deliver the notice in person, or 30 days notice by sending the notice by registered mail to your last known address. The 30-day period starts on the second day after we mail the registered letter. The notice will inform you that you have until noon of the business day before the last day of the notice period to pay the arrears, plus an administration fee, failing which the policy will automatically be cancelled effective at 12:01 a.m. on the last day of the notice period. If you pay the arrears and the administration fee in time, then your policy will not be cancelled

[44] Section 1.7.3 uses the word “must” to underscore the mandatory nature of the insurer’s obligation to provide written notice within the specified time period as a pre-condition to cancellation of a policy of insurance for non-payment of premium. Similar language is not employed in s.6.6, which simply states, “If we choose to do this [i.e., to repair the vehicle], we will let you … know in writing …”. The word “must” does not appear in s.6.6. Moreover, the insurer’s undertaking to provide written notice of its election plainly relates to notice of the election after it has been made. Written notice is not a pre-condition to the election taking effect.

[45] Deputy Judge Da Silva therefore correctly concluded that Certas’s right to repair Ms. Zheng’s vehicle was not vitiated by its failure to comply with the written notice requirement in s.6.6 of the OAP.

[46] It should be noted that Ms. Zheng was in no way prejudiced by Certas’s failure to provide her with formal written notice of its election to repair her vehicle. Despite the absence of written notice, she did receive actual notice of the election within the seven day period after the accident. Certas verbally communicated to Ms. Zheng its decision to repair her vehicle. During her examination-in-chief, Ms. Zheng recalled the first telephone conversation that she had with a Certas representative after the accident. She testified that she was told she would not need to pay the deductible because the accident was not her fault. She recalled that she was also told that “they would be – try to fix my vehicle”. A few days later, Certas advised Ms. Zheng of the appraiser’s conclusion that the vehicle was repairable. Certas confirmed that the repairs would be undertaken at Certas’s expense and Ms. Zheng authorized the work to be done by the body shop.

[47] Ms. Zheng submits that an insurer’s election to repair a vehicle requires the insurer to “take control of the vehicle and get it repaired themselves” because s.6.6 of the OAP states, “We will complete the work within a reasonable time …”. She argues that Certas did not take control of her vehicle and did not complete the repair work on her vehicle, hence it must not have made an election to repair pursuant to s.6.6 of the OAP.

[48] This proposed interpretation of s.6.6 is not one that an ordinary person would adopt. Ordinary people are well aware that insurance companies are not in the business of conducting auto body work or mechanical automotive repairs. An ordinary purchaser of automobile insurance would not reasonably interpret the final sentence of s.6.6 to mean that their insurer would actually take possession or control of their vehicle and complete any necessary repairs.

[49] For the above reasons, I reject Ms. Zheng’s submissions regarding the interpretation of s.6.6 of the OAP. Deputy Judge Da Silva did not employ an incorrect interpretation of s.6.6 when he concluded that Certas had exercised its right of repair. He did not commit an error of mixed fact and law.

[50] Ms. Zheng argues that even if Deputy Judge Da Silva correctly concluded that Certas exercised its option to repair her vehicle that does not preclude her claim for damages for diminished value. I disagree. Deputy Judge Da Silva correctly interpreted the word “rather” in s.6.6 of the OAP to mean “either or”. Once Certas elected to exercise its right to repair Ms. Zheng’s vehicle “rather than pay for the damage”, it was only responsible for the cost of the repairs, up to a maximum of the actual cash value of the vehicle at the time of the accident (per s.6.2 of the OAP). Its contractual obligation was simply to repair the vehicle, which it did.

Accordingly, whereas an insurance may exercise the right to repair a damaged automobile by repairing or replacing parts with a like kind a quality as existed prior to the accident, such is the extent of the obligation of the insurance company. The result is that an insurance company is without an obligation to provide compensation for the devalue arising from the stigma that arises for an automobile with an accident experience.

Statute Barred Lawsuit, including contract exception

As above per Clarendon, among other cases cited above, as well as section 263(5) of the Insurance Act, what is known as the 'no-fault' system is really a system that does still involve a finding of fault or blame for who caused an accident; however, in regards to claiming for damage to an automobile involved in an accident, the right to bring a lawsuit against the blameworthy person is statutorily barred. Despite the lack of right to sue the person who caused an accident, attempts to bring claims against the blameworthy person do occur. These attempts generally happen when:

- The person without blame is without insurance and thus without recourse to claim against the insurer of the automobile;

- The person without blame feels that the insurer of the automobile failed to pay 'enough' and the shortfall is sought against the blameworthy driver; and

- The person without blame seeks compensation for the reduced value of the automobile due to the stigma of an 'accident experience'.

Regardless of these, or perhaps other reasons, it is statutorily forbidden to bring a tort law case containing negligence allegations for damage or other losses to an automobile against the person who is blameworthy for causing the accident. However, per the very well articulated case of Hafeez v. Sunaric, 2015 ONSC 4065 there are exceptions to section 263(5) of the Insurance Act that allow a lawsuit against the blameworthy driver, or another person, who contractually agreed to pay for damage to an automobile damaged via an accident. As is clear from the case law, while section 263(5) of the Insurance Act may forbid legal action on the basis of tort law, legal action is possible when based on contract law. Such a contract may even be enforceable when the agreement is established after the accident occurred and is known to the agreeing persons. Specifically, within Hafeez it was stated:

[16] I also conclude that Judge Godfrey erred in concluding that Mr. Hafeez’s claim was barred by s. 263(5) of the Insurance Act.

[17] The Legislature enacted s. 263 to replaced the tort system and subrogation for property damage claims and brought in a direct compensation regime for property damage claims where an insured makes property loss claims against its own insurer: Siena-Foods Ltd. v. Old Republic Insurance Co. of Canada, 2012 ONCA 583 at para. 18.

[18] In Clarendon National Insurance v. Candow, 2007 ONCA 680 at paras. 7-11, Justice Juriansz explained the direct compensation scheme:

7. Section 263 of the Insurance Act replaced the tort system that resolved automobile damage claims prior to its enactment. In the new statutory scheme, insureds can no longer sue the tortfeasor driver whose negligence has caused damage to their cars. Rather, their own liability insurer pays for the damage, to the extent that they were not at fault, under the third party liability section of their motor vehicle liability policies. Insureds can recover the at-fault portion of their damage by purchasing collision coverage. Insurers have no right of subrogation for payments to their own insureds, but, on the other hand, do not have to pay the subrogated claims previously brought by other insurers in the tort system. The result is that the statutory regime eliminates the transactions costs that were inherent in the tort system.

8. Section 263 is the heart of the regime. The section applies when three criteria are met: ….

9. When the section applies, s. 263(2) provides that the insured is entitled to recover property damage from his or her own insurer:

(2) If this section applies, an insured is entitled to recover for the damages to the insured's automobile and its contents and for loss of use from the insured's insurer under the coverage described in subsection 239(1) as though the insured were a third party.

10. Key to the regime is the insured's inability to recover property damage from anyone other than his or her own insurer, except in the very limited circumstances described in s. 263(5)(a.1):

If this section applies,

(a) an insured has no right of action against any person involved in the incident other than the insured's insurer for damages to the insured's automobile or its contents or for loss of use;

(a.1) an insured has no right of action against a person under an agreement, other than a contract of automobile insurance, in respect of damages to the insured's automobile or its contents or loss of use, except to the extent that the person is at fault or negligent in respect of those damages or that loss.

11. In addition, s. 263(5)(b) prevents insurers from advancing subrogated claims for payments they have made to their insureds:

an insurer, except as permitted by the regulations, has no right of indemnification from or subrogation against any person for payments made to its insured under this section.

[19] In McCourt Cartage Ltd. (c.o.b Laser Transport) v. Fleming Estate (Litigation Administrator of) (1997), 1997 CanLII 12297 (ON SC), 35 O.R. (3d) 795 (Gen. Div.) at para. 3, Justice Sharpe explained the effect of s. 263 as follows:

3. Before the enactment of s. 263, the common law tort regime applied to property damage claims. The result was that where an insured had purchased collision damage cover, and where the accident was caused at least in part by the fault of another driver, two insurers became involved. The insured would claim against his own insurer under the collision coverage, and that insurer would assert a subrogated claim against the insurer of the other driver to the extent of the other driver's fault. The intended effect of s. 263 was to remove the insured's right to sue for property damage and to confer the right to claim such losses not caused by the fault of the insured against one's own insurer. In the words of Somers J. in 583809 Ontario Ltd. v. Kay, 1995 CanLII 7080 (ON SC), [1995] O.J. No. 1626, the section was intended

"to bring to an end claims which were really made by one insurance company against another in the names of their respective insureds strictly for the property damage that had occurred in an accident."

[20] Thus, the property loss compensation scheme introduced by s. 263 precludes tort claims. However, claims in contract are not precluded. There is an exception to s. 263(5) for claims in contract.

[21] This exception for contracts is found in s. 263(5)(a.1), and it was noted and explained by Justice Juriansz in Clarendon National Insurance v. Candow, supra at paras. 19-22 as follows:

19. In this case, Mr. Bounthai's liability insurer, American Home, was statutorily required to provide coverage for his property damage because it had filed an undertaking under s. 226.1. Because the undertaking was filed, all three criteria of s. 263(1) are met: Mr. Bounthai's vehicle suffered damage from an accident in Ontario, his vehicle was insured by an insurer that had filed an undertaking with the Superintendent, and another vehicle involved in the accident (i.e. the appellants') was insured by a domestic insurer licensed to undertake automobile insurance in Ontario. Consequently, Mr. Bounthai is entitled to recover for the physical damage to his tractor from his liability insurer, American Home.

20. As the statutory regime applies, Mr. Bounthai's ability to sue in tort is restricted by the provisions of s. 263. Mr. Bounthai cannot maintain a tort action in negligence against the Candows. Section 263(5)(a) prevents him from suing anyone other than his own insurer for damages to his car. Sections 263(5)(a)'s general rule is subject to the exception set out in s. 263(5)(a.1). This exception permits a right of action where an action is brought "under an agreement, other than a contract of automobile insurance". It permits an action in contract and does not permit an action in tort.

21. The exception would apply, for example, where a provision of a lease agreement requires that the lessee return the vehicle to the lessor in an undamaged state. Where the lessee fails to do so, the lessor can bring an action against the lessee in contract: 583809 Ontario Ltd. v. Kay (1995), 1995 CanLII 7080 (ON SC), 24 O.R. (3d) 445 (Gen. Div.); A Plus Car & Truck Rental v. Pun, [1999] O.J. No. 1291 (Div. Ct.). The exception in s. 263(5)(a.1) has been applied also to situations where the defendant has agreed to pay for the damage to the plaintiff's vehicle without the parties resorting to their insurance - in effect a claim on an oral contract. In Harpeet v. Markham (Town of), [2006] O.J. No. 2439 (S.C.J.), P. Gollom Deputy J. observed at para. 17 that the exception in 263(5)(a.1) "expands causes of action against a person involved in the incident provided the person has entered into a contract, and the person is at fault or negligent." McClinton v. Estien, [2003] O.J. No. 5680 (S.C.J.), is another such case.

22. In this case, however, Mr. Bounthai's action is not brought "under an agreement". Mr. Bounthai's claim is a tort claim that falls within the general rule of s. 263(5) so it is statutorily barred.

[22] As noted by Justice Juriansz, the exception found in s. 263(5)(a.1) has been applied to situations where the defendant agrees by an oral contract to pay for the damage to the plaintiff's vehicle without the parties resorting to their insurance. The case at bar raises the question of whether s. 263(5)(a.1) applies where that defendant agrees by a written contract to pay for the damages to the plaintiff’s vehicle without the parties agreeing to waive their rights to resort to the insurance coverage they paid for.

[23] In the case at bar, Judge Godfrey, in effect, concluded that the exception for contracts found in s. 263(5)(a.1) applied only if the parties agreed not to resort to any insurance coverage.

[24] I, however, see no reason to interpret the exception for contracts in this restricted way. The idea behind s. 263(5)(a.1) is that where there is insurance coverage under s. 263(1) for the damages to the plaintiff’s vehicle and the plaintiff takes advantage of that insurance coverage, then the insured (and his or her insurer by subrogation) cannot sue in tort, but the insured is not precluded from suing for contract claims.

[25] In the case at bar, the handwritten agreement was a contract to pay for the damages to Mr. Hafeez’s vehicle, and, in my opinion, the Insurance Act does not preclude and indeed allows Mr. Hafeez to sue on the contract.

[26] In Brouwer v. Frankel, 2004 CanLII 66346 (ON SC), [2004] O.J. No. 5965 (Sm. Cl. Ct.), the defendant Allen Frankel was driving his family’s car when he was involved in an accident with the plaintiff Tara Brouwer’s vehicle. Mr. Frankel’s mother came to the scene of the accident and agreed to pay the cost of repair to the Brouwer vehicle if two estimates were obtained. After Ms. Brouwer had her vehicle repaired, the Frankels refused to pay, and they argued that Ms. Brouwer’s claim was barred by s. 263(5)(a.1) of the Insurance Act. In that case, Judge Godfrey disagreed with the Frankels’ argument, and held that the contract claim against them was available. He stated at paras. 3-6:

3. The defendant relies on section 263(5)(a.1) of the Insurance Act as barring an action against the defendant. The defendant's agent alleged that this clause is applicable because the prerequisites in section 263(1) have been met. The defendant's agent is correct that clauses (a), (b) and (c) of section 263(1) are applicable to the accident in question.

4. Does section 263(5)(a.1), however, bar the plaintiff's action? Section 263(5)(a.1) was added to the Act by Bill 59 in 1996. Prior to its introduction, section 263(5)(a) would have been the only apparent possible restriction in the plaintiff's recovery against the defendant. This clause prevents an insured from maintaining a cause of action against "any person involved in the incident other than the insured's insurer for damages to the insured's automobile".

5. The defendant was not involved in the incident. The defendant merely arrived after the fact, and made a contract with the plaintiff in order to avoid reporting the accident to the owner's insurance company. Accordingly, without the existence of section 263(5)(a.1), the plaintiff could clearly sue the defendant in contract.

6. Was the purpose of section 263(5)(a.1) to prevent the insured from suing persons not involved in the incident? From my reading of section 263(5)(a.1) the purpose of that section was to create an additional cause of action for the insured against those involved in the incident provided the person at fault for the accident agreed to pay for the damage. The 1996 amendment appears to have been created to expand an insured's right to bring an action, and not for the purpose of narrowing a previously existing right. Although the right of the plaintiff to a cause of action in these circumstances is not abundantly clear from the legislation, I find that the plaintiff's right to sue the defendant exists upon considering section 265 in its entire context. In other words, the amendment is not intended to exclude collateral contracts with third parties not involved in the incident. The amendment expands causes of action against a person involved in the incident provided the person has entered into a contract, and the person is at fault or negligent.

[27] I agree with Judge Godfrey that s. 263(5) does not bar claims in contract against third parties not involved in the accident who agree to pay for the property damages. I also agree that s. 263(5) does not bar a contract claim against a person involved in the accident provided the person has entered into a contract, and the person is at fault or negligent.

Accordingly, the case law well shows that a tort claim brought against the negligent driver who caused an accident and caused damage to other automobiles will be precluded by operation of section 263(5) of the Insurance Act; however, if the negligent driver contractually agreed to pay for damage arising from such negligence, a claim in contract law should be permitted.

Summary Comment

Automobile insurance can be complicated if viewed as a whole with an attempt to digest a complete understanding all at once; however, the task is made much easier by compartmentalizing the various coverage sections for the intent, purpose, and protection, that each section offers.

As for the coverage sections applicable to damage to an automobile occurring within an accident, being Direct Compensation Property Damage, Uninsured Automobile, and Collision, understanding of each can also occur much more easily when digested separately. Each coverage possesses unique and often unexpected quirks.